30/12/2025

22/12/2025

PFRDA has introduced 2 new investment pattern schemes viz Life Cycle 75 - High (15E/55 Y) and Life Cycle Aggressive (35E/55Y) for both the NPS and UPS Subscribers. Accordingly, interested subscribers can choose out of them voluntarily so as to gain more from higher equity portion exposure.

17/12/2025

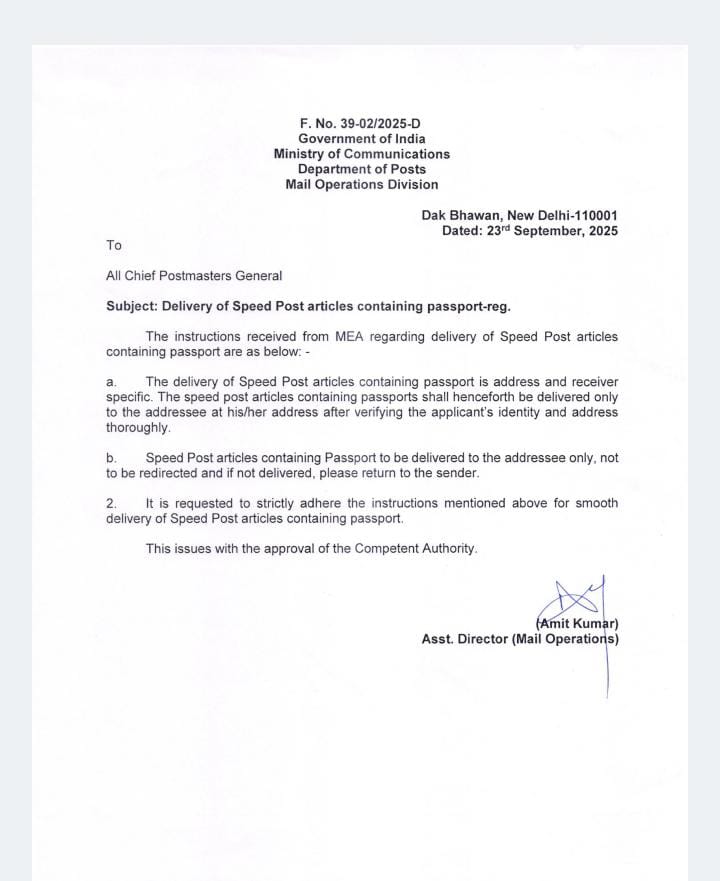

Implementation of revised volumetric weight formula for domestic parcels

Submission of AIPR under Rule 18 of Central Civil Services (Conduct) Rules, 1964

Processing of Unaccountable in Single processing Hubs

Circle Conference of Punjab Circle held on 18.11.2025.

Circle Conference of Punjab Circle was successfully held at Firozpur. I had the opportunity to attend the meeting, and on behalf of the CHQ, A special congratulations to Shri Kanwaljeet Singh, who has been re-elected as the Circle Secretary and extend my heartfelt wishes to the newly elected office bearers of Punjab Circle.

15/11/2025

Representation of 8th CPC for Central Government Employees.

On behalf of FNPO, we proposed modifications to the Terms of Reference (ToR), particularly concerning pension review/revision, minimum wage, fitment factor, allowance revision, and other related matters. We suggested that a common consolidated report be prepared through a separate drafting committee.

FNPO also submitted a letter requesting the inclusion of GDS under the purview of the 8th CPC.

A drafting committee will prepare its report based on inputs from all stakeholders by 15.12.2025. FNPO will nominate one official to serve on the 8th CPC Drafting Committee.

With regards

Sivaji Vasireddy Secretary General FNPO

11/11/2025

FNPO suggestions in 13th PSS welfare board.

On 11.11.2025 SIVAJI VASIREDDY, SG FNPO Participated in The POSTAL SERVICES WITH IN BOARD (PSSWB) HELD UNDER THE CHAIRMANSHIP OF SRI JOTHIRADITYA SINDYA HONORABLE MOC, SECRETARY POST, DG POST, MEMBER WELFARE, CPMG'S Of DELHI, MAHARASHTRA, MP, GUJARAT AND OTHER OFFICERS.SG FNPO requested the honorable minister to provide some specific quota in departmental exams for GDS who are showing their excellence in sports. MoC sir agreed to the proposal and also directed the secretary to arrange a meeting with GDS who showed good performance in previous postal sports events. Some other welfare issues were also discussed and MoC sir assured to hold separate meetings again to resolve all. The following proposals amend various welfare allotments. Please find details of the approval.

On 11.11.2025 SIVAJI VASIREDDY, SG FNPO Participated in The POSTAL SERVICES WITH IN BOARD (PSSWB) HELD UNDER THE CHAIRMANSHIP OF SRI JOTHIRADITYA SINDYA HONORABLE MOC, SECRETARY POST, DG POST, MEMBER WELFARE, CPMG'S Of DELHI, MAHARASHTRA, MP, GUJARAT AND OTHER OFFICERS.SG FNPO requested the honorable minister to provide some specific quota in departmental exams for GDS who are showing their excellence in sports. MoC sir agreed to the proposal and also directed the secretary to arrange a meeting with GDS who showed good performance in previous postal sports events. Some other welfare issues were also discussed and MoC sir assured to hold separate meetings again to resolve all. The following proposals amend various welfare allotments. Please find details of the approval.Revision in various Welfare Schemes.

04/11/2025

8th CPC Gazette notification.

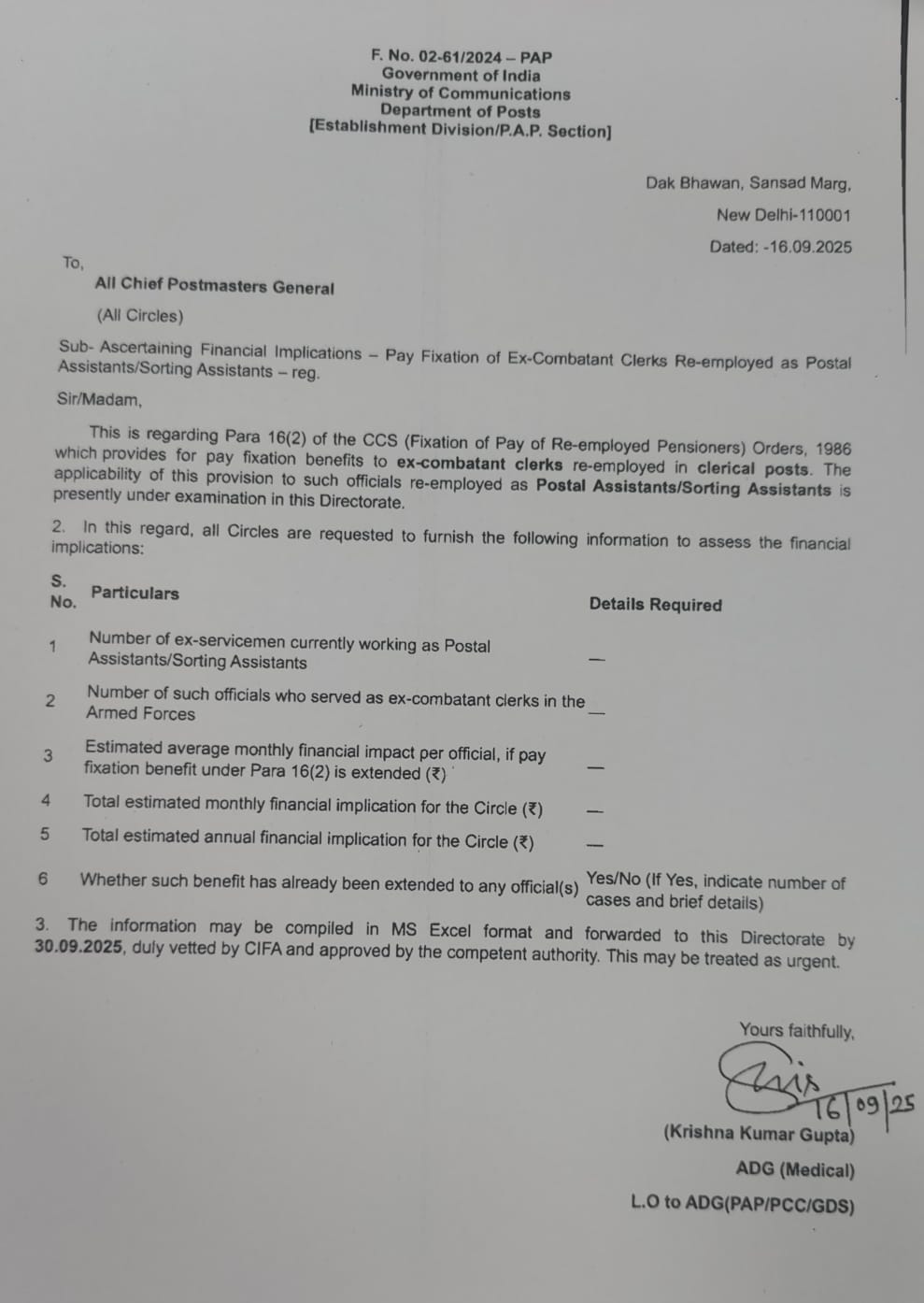

Information on financial implications regarding applicability of Para 16(2) of CCS (Fixation of Pay of Re.employed Pensioners) Orders, 1986 to ex-servicemen re-employed as PAs/SAs.

Additional Charge on the vacant posts of the Higher Administrative Grade of the Indian Postal Service, Group ‘A’ in Postal Circles/Postal Directorate.

05.10.2025

Our Homage to our beloved & respectable Leader K.R.

Let us remember K.R. Today on his 30th death anniversary. The below statement is approved by the Ministry of Communication on his 100th Birth Centenary.

Let us follow K.R footsteps.

K. Ramamurthy was born on 08.08.1912 in Tirunelveli, Tamilnadu. He was the Secretary General of U.P.T.W. and also the Secretary General of Central Government Employees Union Federation. K. Ramamurthy was the architect of the NFPTE and also founder of FNPTO. He tendered evidence to all the five Pay Commissions. K. Ramamurthy was nominated as member of P&T Joint Committee of the ILO in 1984. In fine K. Ramamurthy was an embodiment of staunch Unionist and true Nationalist.

our ever respected P.M, Indra Gandhi taking a cup of Tea with our KR.

15.09.2025

On 15.9.25 second meeting of Cadre review case of PA PO, PA CO/RO and SA in RMS under the Chairmanship of Sri K.Praksh CPMG Karnataka. On behalf of FNPO Sivaji Vasireddy, S.Khandoji Rao CS NAPEc Karnataka, R.Murali CS NUR3 Tamilnadu, Chandrasekhar, CS NUR3 Karnataka attended physically and NK Tyagi GS NUR3 virtually.

13.09.2025

Federal Working Committee Meeting

The Federal Working Committee Meeting of the Federation was held from 12.09.2025 at the YMCA Hostel Conference Room, New Delhi, under the chairmanship of the Secretary General. The meeting was attended by all Federal Executive Committee Members.

The Secretary General presented a comprehensive draft report covering various developments on organizational matters and issues currently being faced by Postal Employees across India.

From the RMS side, the following leaders participated:

Shri N. K. Tyagi, General Secretary

Shri U. M. Mhaskar, Deputy Secretary General

Shri Rabindra Patnaik, Federation Vice President

Shri Sube Singh, ASG & Circle Secretary, Delhi Circle

Shri S. M. Bhandari, Federal Councillor (MMS)

The following key issues were jointly discussed and pressed upon by the RMS representatives:

1. Reduction of offices since MNOP (2010) – highlighting the drastic cut-down in operational units.

2. Hubs at the time of MNOP introduction – 93 NSH, 2 APS, 148 ICH, and 225 CRCs.

3. Position as of December 2024 – post-merger, reduced to 95 NSH, 2 APS, and 163 ICH.

4. Introduction of MPOP – Department’s plan (based on McKinsey recommendations) to further reduce hubs to 41 NSH and 122 ICH.

5. Union’s strong opposition – demanded federation action against officers responsible for arbitrary amalgamations.

6. Last MPOP meeting minutes – discussion and demand for ATR.

7. Cadre Restructuring of Sorting Assistants (SA) – concern over intentional delays; urged federation to forward the already-prepared report to DoP&T immediately, without linking it unnecessarily to PA Cadre Restructuring.

8. Cadre Restructuring of MMS – finalized proposals should be implemented at the earliest. Shri S. M. Bhandari also emphasized changes in Recruitment Rules and promotion percentages for MMS cadres.

9. 8th Pay Commission – condemned inordinate delay in constitution of the committee; stressed formation of a union-level committee.

10. APT 2.0 issues – detailed problems raised by Circles; demanded urgent meeting at Directorate.

11. Constitution of JCA – urged federation to form a Joint Council of Action of all unions, and issue notice if necessary to oppose anti-worker policies, with support of PJCA if required.

12. Policy matters by Secretary General – assurance given for corrective action on all fronts.

13. PA–SA Merger issue – detailed discussion on possible departmental move; strategy to be adopted was deliberated.

14. Next Federal Congress – proposed to be held at Himachal Pradesh in May 2026.

15. Overall outcome – meeting was conducted in a cordial atmosphere with fruitful discussions among Postal and RMS unions.

Subscribe to:

Comments (Atom)